This kind of home loan is best for individuals who have bad credit or who do not have enough cash for a traditional 20% down payment. However, it does come with a rate: higher monthly payments! When a house owner has to pay less than the standard 20% down payment on a home, they usually have to acquire personal mortgage insurance since they're a high risk borrower.

With a FHA home loan, the borrower should pay 1.75% of the house's value in advance, and after that a month-to-month charge called a Yearly Home loan Insurance Premium. This month-to-month charge depends on the loan size and length of loan. Although this home loan does not need one, having a home warranty strategy is a good idea to safeguard your home's systems and devices.

This is a traditional mortgage that you can certify for with a bank or cooperative credit union. This home loan might be a fixed rate or adjustable, however does require a greater credit history, normally above 600. A house warranty strategy is another excellent idea for this home loan option. In the previous loans, a borrower paid a month-to-month payment on the interest and the premium.

9 Easy Facts About What Percentage Of National Retail Mortgage Production Is Fha Insured Mortgages Shown

This indicates that the initial regular monthly payments are exceptionally low, but will jump up when the interest is settled. Nevertheless, you're not constructing equity in your house, and you'll be paying much more interest than if you try and pre-pay a fixed-rate home mortgage. Rather of looking into an interest just loan, have a look at some home warranty plans in your location.

A jumbo home mortgage is any loan above $625,500, while a conforming home mortgage is any loan below that. A VA loan is only for those people who are actively serving in the military, veterans or some spouses. The Department of Veteran Affairs will back loans from banks or mortgage companies to offer housing for military workers.

To find out more on house warranty plans go to www.landmarkhw.com. You can compare our house service warranty strategies and prices here..

Which Mortgages Have The Hifhest Right To Payment' Can Be Fun For Everyone

So, you are thinking of buying a house. which of the following is not an accurate statement regarding fha and va mortgages?. Prior to you even begin looking at property options, you need to do your research about the various kinds of home mortgages that are readily available through Tucker Home loan and other monetary specialists. Ratings of home loan products are https://www.pinterest.com/wesleyfinancialgroup/ available in the contemporary market-- however how do you arrange through them all? Our quick and simple guide can assist you find out about the various kinds of home loans that are presently offered to property buyers, helping you make the right decision for your current and future financial plans.

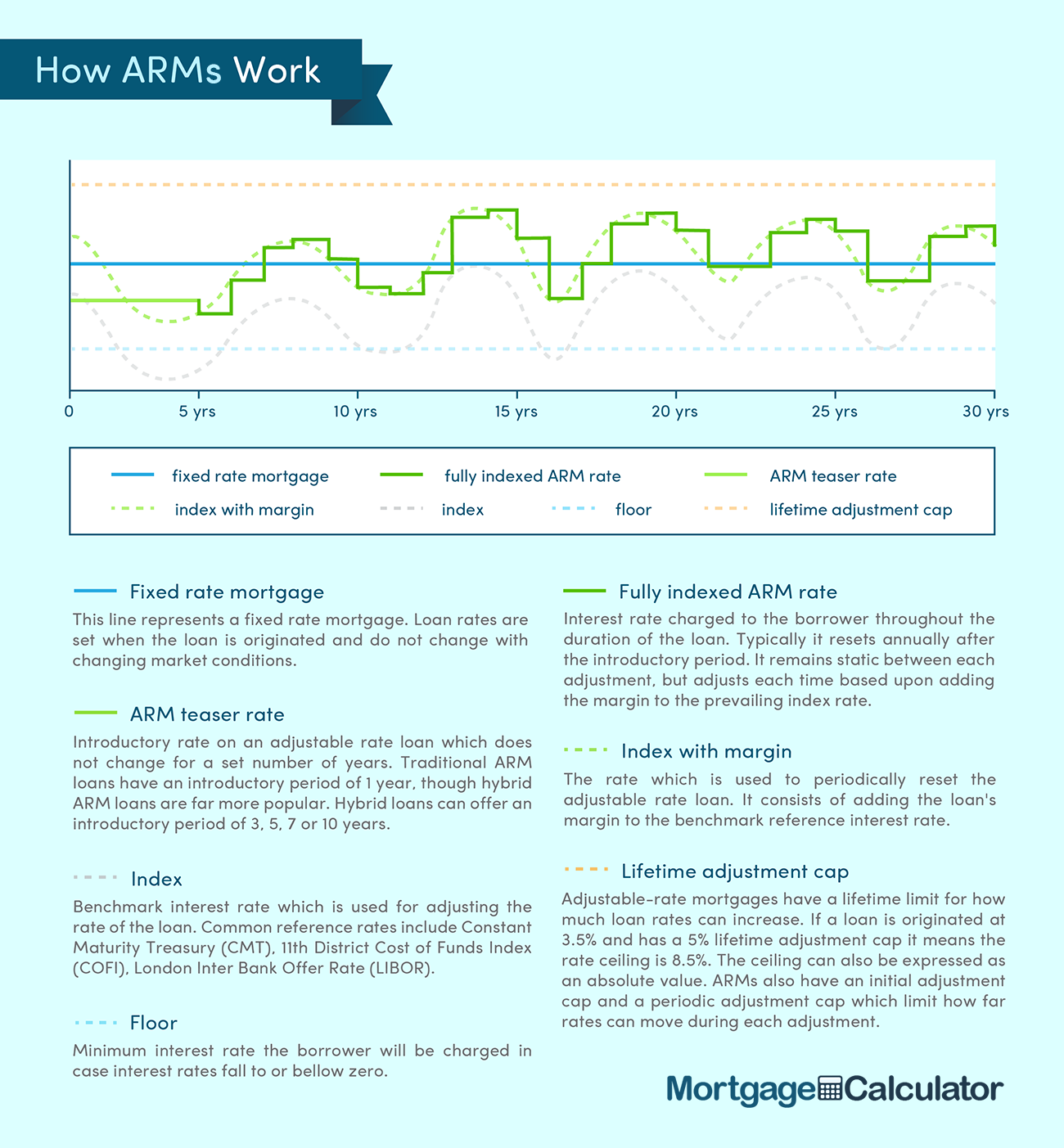

This simply indicates that you are choosing a mortgage loan that is not insured by the federal https://www.businesswire.com/news/home/20190911005618/en/Wesley-Financial-Group-Continues-Record-Breaking-Pace-Timeshare government. Traditional loans consist of a variety of different loan plans, consisting of fixed-rate and adjustable-rate, together with hybrid ARMs, which we will talk about throughout this document. Conventional loans generally require a 5 percent down payment.

Conventional home mortgages are administered completely through financial institutions such as banks. These conventional loans may be guaranteed by personal entities to lower the danger of financial losses by the bank or lending organization. Nevertheless, not all standard loans are insured. Borrowers who are seeking loans greater than 80 percent of the residential or commercial property value will generally require personal home mortgage insurance coverage (PMI), however a big down payment might exempt the debtor from that guideline.

The Single Strategy To Use For What Are The Different Options On Reverse Mortgages

This is especially convenient for borrowers who are aiming to finance their 2nd house or perhaps buy an investment property. A conversation with your lender can help identify whether you require loan insurance. In contrast to traditional home mortgages, Federal Real estate Administration, or FHA loans, are guaranteed by the federal government, though they are still administered by banks.

For example, FHA loans usually require a smaller sized deposit-- typically as low as 3.5 percent-- which allows own a home to be more available to buyers with lower earnings. FHA loans are developed to assist people who might not otherwise think about themselves as property owners! However, these FHA loans typically come with greater rate of interest, which can end up costing more over the regard to the loan.

Interest rates for FHA home loan can change regularly, depending upon updates to the standards that are set by the Federal National Home mortgage Association, also called Fannie Mae. These standards include the "adhering limitation," which is the maximum worth of a loan that Fannie Mae and its sibling firm, Freddie Mac, will buy.

Why Do Holders Of Mortgages Make Customers Pay Tax And Insurance Things To Know Before You Buy

Nevertheless, these standard loans may not be as quickly readily available to those who are restricted by lower earnings. A lot of home mortgage that are written in the U.S. come from either a conventional or FHA home mortgage sources. Start by figuring out which of these classifications is ideal for you before you begin taking a look at payment structures and loan specifics.

They are relatively simple. Your fixed-rate home mortgage will always have the very same rates of interest, no matter what the financial landscape looks like in your area, or in the country overall. The advantage, obviously, is that it is much simpler to prepare your financial future with a loan that uses stability and predictability.

Much shorter home mortgage terms from Tucker Mortgage permit you to settle your home much faster and construct that critical house equity, but your regular monthly payments will be higher. So, why should you pick a set rate home mortgage? You would probably be an excellent candidate if you plan to remain in your house for lots of years; you might even plan to pay it off completely without selling.

School Lacks To Teach Us How Taxes Bills And Mortgages Work Fundamentals Explained

Purchasers also require to examine the financial climate; if they believe this is a "great" interest rate compared to the norm, they must most likely think about a fixed-rate home loan with Tucker Mortgage. You might be delighting in smaller sized payments while people with other loans are struggling to comprehend and accommodate their variable rates!The most typical term for a fixed-rate mortgage is the 30-year choice, though this type of home mortgage can take as little as 15 years to settle-- and often they can even be extended to 40 years! It is crucial to remember the fact that the total quantity of interest you pay is more dependent upon the length of the home mortgage instead of the rates of interest itself-- an extra 10 years of payments can amount to 10s of countless dollars!Fixed- rate home loans are eventually best for those people who mean to stay in their house for a long period of time and who believe that rate of interest will remain stable for the future.

Debtors who are trying to find a larger loan than the federal acknowledged "adhering loan limits" might need to seek out special home loans to accommodate their requirements. In most counties, any mortgage above $417,000 will need unique terms, likewise referred to as a jumbo loan (how to rate shop for mortgages). In higher-cost locations, that federal limit may be raised into the $600,000 range.

Professionals in the industry say that debtors who are trying to find these high-end home loans generally wish to purchase a home in the variety of $750,000 to $10 million, with most of those loans valued at $2.5 million and above. Jumbo loans generally cover amounts as much as $1 million that go beyond the federal requirements.